College Savings, Explained

529 basics and key takeaways

This post is part of a 3-part series inspired by our recent Smarter Savings Association webinar with David from the DC College Savings Plan.

Part 1: Key takeaways + 529 basics (you are here)

Part 2: The practical playbook (how to start, contribute, and use funds well)

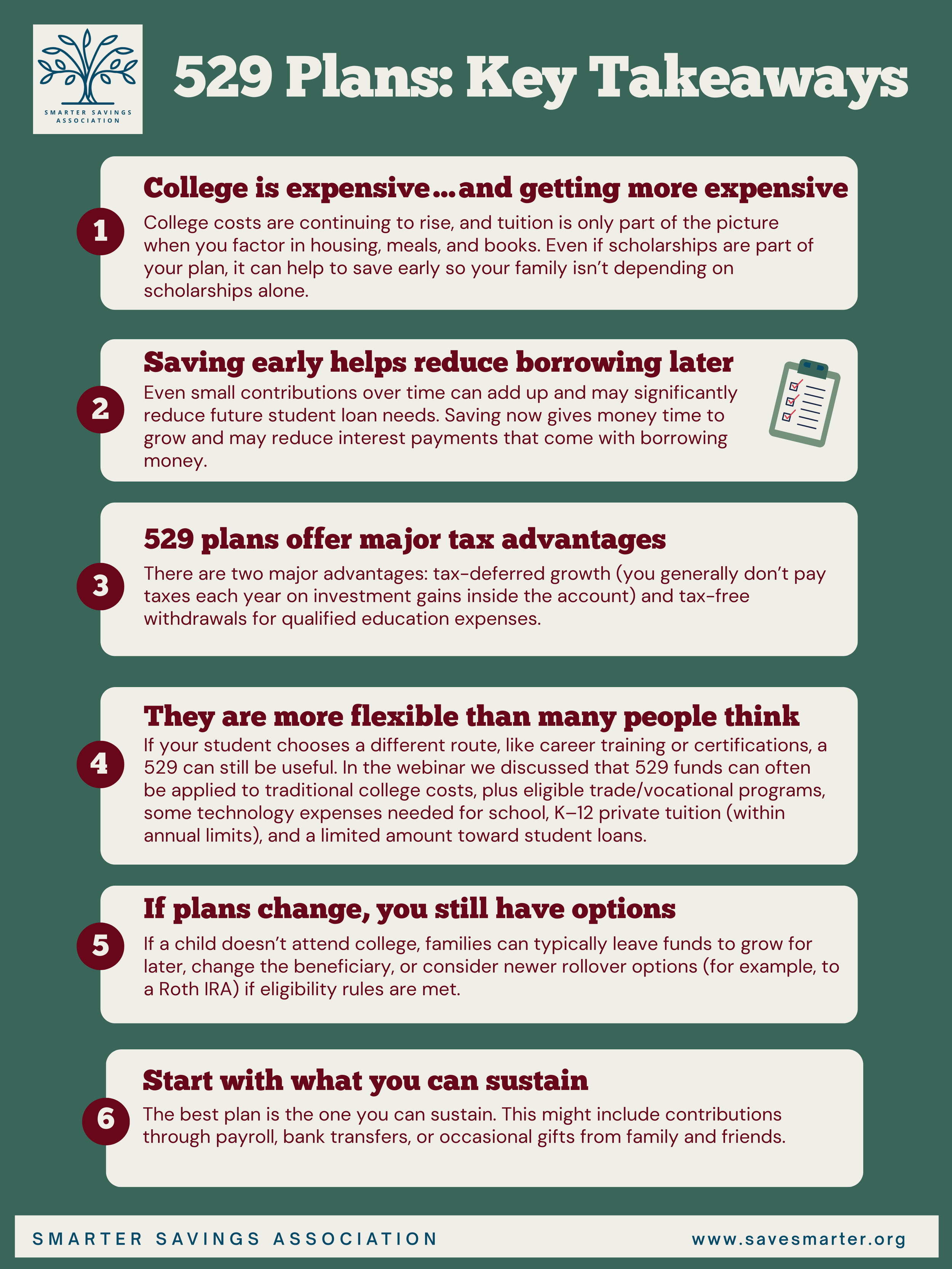

Key takeaways from the webinar

A recent Smarter Savings Association webinar with the DC College Savings Plan focused on one core reality: college costs are rising fast, and even “good” scholarships often leave families with a sizeable gap. 529 plans can help families save in a tax-advantaged and flexible way, starting with whatever amount is manageable. The key takeaways?

SSA members can download this one-page guide in the member portal. Education only; not tax or investment advice.

What is a 529 plan?

A 529 plan is a dedicated education savings account designed to help families set aside money for education expenses. It is commonly used for college savings, but it can also support other eligible education pathways.

Most people are drawn to 529 plans for three reasons:

Tax advantages - how savings can grow and be withdrawn.

Flexibility - how funds can be used and adapted if plans change.

Control - the account owner retains control of the funds.

This series will go deeper on each one, but here is the big picture.

How 529 plans work

You open an account (as the “account owner”) and name a beneficiary (the student). You contribute money over time. The funds can be invested, and the account may grow. When it’s time to pay for eligible education expenses, you withdraw funds to cover those costs.

Two important concepts from the webinar that are worth repeating:

Time helps. Starting earlier, even with smaller contributions, can increase what you build over time.

A 529 is not “all or nothing.” Many families use it alongside other resources (cash flow, scholarships, financial aid, grants, and sometimes borrowing).

Top 529 plan benefits: tax advantages and flexibility

1) Tax-deferred growth

In many cases, investment earnings in a 529 can grow without annual taxation while the money remains in the account.

2) Tax-free qualified withdrawals

When withdrawals are used for qualified education expenses, the distributions can be tax-free at the federal level and may also be tax-free at the state/local level depending on the plan and residency rules.

3) Flexibility when plans evolve

One of the biggest “aha” moments from the webinar was how many different education paths a 529 can support, and what families can do if their child’s plans change.

(We’ll cover “what counts” and “what happens if…” in more detail in Part 2.)

Common myths…and what to know instead

Myth: “My child will get a scholarship, so I don’t need to save.”

Scholarships can be helpful, but they do not always cover full costs. Many families still face a gap.

Myth: “A 529 is only for traditional four-year college.”

The webinar discussed additional eligible uses (including certain vocational/trade pathways, and other qualified expenses), subject to program rules.

Myth: “The money becomes the child’s at 18.”

In general, the account owner controls how and when funds are used for eligible expenses.

Myth: “If my child doesn’t go to college, I lose the money.”

Families may have options, including changing beneficiaries or other permitted strategies depending on circumstances and eligibility requirements.

Click here for Part 2, the Practical Playbook, where we walk through a 7-step guide on setting up and using a 529.