Build a Budget That Allows You to Save Money: Budgeting Basics

This is the final part of our Budgeting Basics series. If you're just joining us, start with What is a Budget? and work your way through, or jump to any step that feels most relevant to where you are right now.

You've done the hard work. You know where your money is going. You've sorted your wants from your needs. You've prioritized what matters most. You've even thought about how your budget fits your life.

Now it's time to make sure saving is part of the plan, not just what's left over at the end of the month.

Why Saving Gets Skipped

For a lot of people, saving happens last, after the bills are paid, groceries are in the fridge, extras are covered... maybe put something aside if there's anything left. The problem? There might not be anything left. If saving comes last, it becomes much harder to do (if at all).

Pay Yourself First

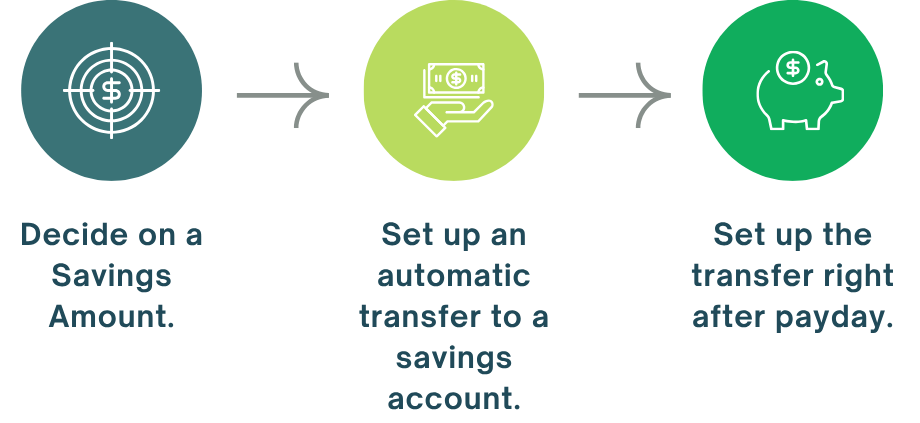

The simple fix: treat saving like a bill. Before you spend on anything else, move money into savings.

This doesn't have to be a big amount. Even $10 or $20 a paycheck adds up over time. What matters is that saving happens automatically, before you have a chance to spend it somewhere else.

Here's how to make this happen in three steps:

Where Should the Money Go?

That depends on your goals. A few options:

Emergency fund — Money set aside for unexpected expenses like car repairs or medical bills. Aim to have $500 to start, then build toward 3–6 months of expenses over time.

Short-term goals — Saving for something specific like a trip, a new phone, or a security deposit.

Long-term goals — Retirement, a house, your kid's education. These usually go into separate accounts like a 401(k) or 529 college savings account.

You don't have to save for all of these at once. Pick one to start.

How Much Should You Save?

You may have heard the advice to save 20% of your income. That's a fine goal, but it's not realistic for everyone, especially if you're just getting started.

Here's a better approach: save what you can, then increase it over time.

Start with 5% (or even less)

Every few months, bump it up by 1%

Adjust when your income changes

The goal isn't perfection, the goal is progress.

What If There's Nothing Left to Save?

Go back to your priorities. Look at your wants. Is there one small thing you can pause or cut back, just for now, to free up money for savings? This isn't about deprivation, it's about trade-offs.

Sometimes we spend on things that don't actually matter that much to us, just out of habit. A quick review of your spending can reveal where there's room. Look back at our wants vs. needs and prioritize your spending posts to dive into this further.

Saving Is a Habit

The first transfer is the hardest. After that, it gets easier. Once saving becomes automatic, you stop thinking about it and your savings start to grow. Remember, the most important step is just to start!

You Did It

If you've followed this series from the beginning, you now have everything you need to build a budget that works for your life:

You've reflected on how to build a budget that fits your lifestyle

And now, you're making saving part of the plan

This series is designed to help you think about what budgeting looks like for you in real life. Your budget is going to look different than your best friend's or your sibling's, and it should! A budget that reflects your values and the things that matter most to you is one you'll actually stick to.

As you build and follow your budget, there will be weeks or months that don't go as planned and that's OK. The goal isn't perfection, it's to keep going, even when things don't work out the way you expected.

If you're a member, head to the online worksheets page to put these steps into action. And if you're not a member yet, join us to get access to all our budgeting tools.